The Society for Worldwide Interbank Financial Telecommunication (Cross-border) and the Single Euro Payments Area (SEPA) are two main international payment schemes for sending cross-border transfers. These play a vital role in the global financial system. Here’s some evidence to support this statement:

According to Statista, the number of Cross-border payments processed daily reached nearly 50 million messages.

As of 2024, instant payments account for approximately 12% of SEPA’s total credit transfer volume. Projections suggest that, with favorable regulatory changes, this could rise to 45% by 2027, significantly increasing from the current levels.

This article explores the key differences and similarities between the two payment schemes. Both systems have evolved to meet the demands of global commerce and streamline international transactions. Understanding their unique features and how they cater to different audiences can benefit businesses and individuals in today’s interconnected world economy.

What is Cross-border?

Cross-border is a system that banks worldwide use to send money and messages to each other safely. It’s like a special service helping banks communicate clearly and securely. Banks use a special code to identify each other in this system, ensuring the money reaches the right place.

This system is used for many bank transactions, including transferring money from one country to another. It’s known for being reliable, which means people can trust it to handle their money transactions without problems. Cross-border is a vital tool in the global banking world, helping to keep money moving smoothly and safely between banks in different countries.

What is SEPA?

SEPA is a system that makes sending euros between European countries easier. It was created to make all euro payments in this area as simple as paying within one’s own country. This means that whether someone transfers money to a family member in another country or makes a business transaction, it can be done quickly and easily, just like a local transfer.

SEPA covers credit transfers (like online payments), direct debits (automatic withdrawals), and card payments, making it a one-stop solution for various transactions. It’s a step towards making Europe’s financial system more united and efficient, ensuring people and businesses can move money around without fuss.

What are the main differences between Cross-border vs SEPA?

Both are systems that help people transfer money, but they work in different ways and have different features. Here are some key differences between them:

Cross-border

SEPA

Where They Operate

Operates globally, allowing money transfers in various currencies across more than 200 countries.

Focuses on European countries, specifically facilitating euro transfers among 36 member countries.

Scale and Reach

Used by over 11,000 banks and financial institutions globally, making it a widely used network for international transactions.

Primarily a pan-European system, helping to unify and streamline euro transactions within its member countries.

Transfer Details Required:

Requires detailed information, including the Bank Identifier Codes (BIC), Cross-border codes, and other specifics about the recipient’s bank.

Simplifies the transfer process, not necessitating BIC or other intricate bank details for transfers.

Speed and Convenience

The transfer time can be longer, especially involving multiple currencies and several intermediary banks.

Offers fast, convenient, and hassle-free transfers, often completing transactions within a business day.

Usage

Frequently used for various kinds of international transactions, including business and personal transfers.

Primarily used for personal and business euro transfers within the designated European region.

Understanding these differences can help you choose the right service for your needs, whether you want to send money internationally or within Europe. It also helps in planning the transfers more effectively, considering the speed and the information required by each system.

What countries are included in the SEPA zone?

The SEPA countries include the 27 European Union (EU) member states and a few additional countries.

European Union (EU) Member States:

Austria

Belgium

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Ireland

Italy

Latvia

Lithuania

Luxembourg

Malta

Netherlands

Poland

Portugal

Romania

Slovakia

Slovenia

Spain

Sweden

Non-EU Members:

Iceland

Liechtenstein

Norway

Switzerland

Monaco

San Marino

Andorra

Vatican City

United Kingdom

What countries use a Cross-border code?

BIC codes are used by financial institutions in virtually every country worldwide to facilitate international financial transactions. The payment scheme operates in over 200 countries and territories, encompassing a large network of banks and financial organizations globally. The geographical spread where Cross-border codes are used:

North America. Including countries like the United States, Canada, and Mexico.

South America. Encompassing countries such as Brazil, Argentina, and Chile, among others.

Europe. Including nations like the United Kingdom, France, Germany, Spain, etc.

Asia. Incorporating countries such as Japan, China, India, and South Korea, among others.

Africa. Including countries like South Africa, Nigeria, Kenya, and more.

Australia and Oceania. Comprising countries such as Australia, New Zealand, and several Pacific island nations.

Middle East. Including countries like the United Arab Emirates, Saudi Arabia, and Qatar, among others.

How does Cross-border code work?

Cross-border codes play a vital role in international financial transactions. These codes are essentially the addressing system that helps in the smooth and accurate routing of money transfers between banks globally.

Such code is typically an 8 to 11-character alphanumeric code. The first 4 characters represent the bank code, the next 2 characters represent the country code, followed by a 2-character location code, and optionally, a 3-character branch code. This is how it works.

1. Identification of Parties

Sender. A person or entity that wants to send money internationally initiates the transaction, providing the recipient’s banking details, including the Cross-border code of the recipient’s bank.

Recipient. The person or entity that will receive the funds. Their bank’s Cross-border code is required to ensure the money reaches the correct institution.

2. Generation of Cross-border Message

Message Creation. The sender’s bank creates a Cross-border message, which is a standardized format containing all necessary details about the transaction, including the recipient bank’s Cross-border code.

3. Transmission of Cross-border Message

Sending the Message. The message is transmitted through the Cross-border network, a secure financial messaging service, not a funds transfer system.

4. Action by the Recipient’s Bank

Receipt of Message. The recipient’s bank receives the Cross-border message, which contains instructions for the transaction.

Funds Transfer. Based on the instructions in the Cross-border message, the recipient’s bank arranges the transfer of funds from the sender’s bank to the recipient’s account.

5. Completion of Transaction

Notification and Credit. The recipient is notified, and their account is credited with the transferred amount.

Please note, if you already have PayDo Business Account, you can find Cross-border/BIC code following these instructions:

Access your PayDo Account.

In the dashboard, go to Account Details.

Under the Dedicated section you will find your IBAN/Cross-border codes.

Conclusion

Cross-border and SEPA are two prominent systems facilitating money transfers, each catering to different geographical and transactional needs. It is important to understand their key differences:

Geographical Scope. Cross-border has a broader global reach compared to SEPA’s focus on the European region.

Currency. Cross-border facilitates multi-currency transactions globally, while SEPA is confined to euro-denominated transactions.

Speed. SEPA generally offers faster transfer times, especially for transactions within the SEPA zone, compared to Cross-border’s varied transaction speeds.

The choice between Cross-border and SEPA transfers would depend on the transaction’s nature, with SEPA being more suitable for euro transactions within Europe and Cross-border being apt for broader international transactions. Please contact our support team to get information on how to use both SEPA and Cross-border with PayDo.

Starting and running a business is undeniably tough. According to recent statistics, about 10% of new companies fail within their first year and 90% fail over the long term. This...

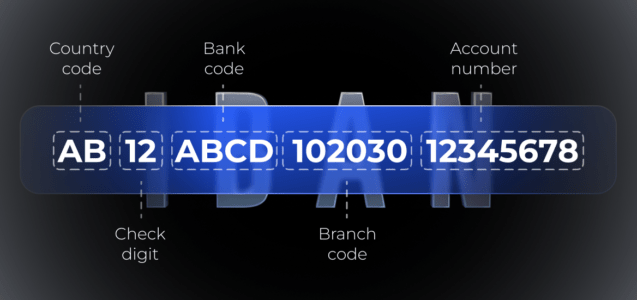

The International Bank Account Number (IBAN) is the standard for international transfers. Today, IBAN account number is used in 88 countries. Before IBAN’s introduction, around 10% of international transfers faced...

As digital payments continue to rise, so does the threat of payment fraud. In 2024, over 50% of banks surveyed by Alloy reported an increase in business fraud, and more...

Digital payments in commerce are growing and evolving rapidly. The fintech-for-commerce market is booming, driven by the demand for faster, more efficient payment processing. Digital and automated B2B payments are...

We have talked at length about the International Bank Account Number (IBAN) – the standard for international transfers. What makes it worth it, how to find it and understand what...

Card transactions not only move money: they also cost money. Every single financial transfer to your business will usually yield a processing fee between 1.5% and 3.5% of the entire...

IBANs (International Bank Account Numbers) are the standards for internal money transfers in many countries, including the entirety of the EU, but Canada relies on a different set of systems...

Visa and Mastercard are currently responsible for more than 90% of all financial transactions taking place outside of China, so a company in need of a business account is likely...

How consumers and companies interact with financial services has changed dramatically in recent decades. The digital banking market reached $9.4 trillion in 2023 and is expected to reach approximately 3.6%...

Imagine each bank branch with its unique postal code — that’s what a branch code or sort code is in the financial world. It’s a set of numbers that stamps...

According to what banks suggest, a high-risk business is the one with a high chance of fraud or chargebacks. In the payments industry, no single organization defines what makes a...

Most banks today offer online banking. This means you can pay bills, make transactions, and see all your activity in real time from your phone, tablet, or laptop. You can...

The Society for Worldwide Interbank Financial Telecommunication (Cross-border) and the Single Euro Payments Area (SEPA) are two main international payment schemes for sending cross-border transfers. These play a vital role...

A Company Registration Number (CRN) is a code a business gets during incorporation. It acts as a distinct identifier for your company. It helps to differentiate your company from others...

Today, it is no longer possible to meet someone who would not know what an online bank account is and what it is needed for. Statista says there are 1.9...

A bank account ownership certificate, also known as a bank account certificate or proof of account ownership, is a document that says your bank account actually belongs to you. It...

When it comes to sending or receiving money internationally, your bank or any other financial institution needs to know precisely where the funds should go. Enter the Cross-border or BIC...

Digital payments are now crucial for the world’s economy. They change how businesses and individuals pay for goods and services within multiple industries. According to a recent report by Statista,...

Globalization and digital services have changed how companies do business, making e-commerce a key tool for buying, selling, and providing services online. The market is expected to reach $6.4 trillion...

The iGaming industry is an economic powerhouse. It generates impressive revenues and fosters innovations. The European iGaming market saw a notable 23% boost in revenue, hitting $115.7 billion in Gross...

“Approximately 4.2 billion gambles at least once a year.” In other words, more than half of the planet is part of the iGaming market, which is developing really fast (see...

The year 2024 has been a real test for many sectors of the economy. However, online payments have only become more popular. Nevertheless, in the near future, online payments will...

You may have heard of these terms and wonder the exact meaning of Cross-border or SEPA, and the essence put in simple words. Yet, often, there are many more such...

Many businesses just want a basic account, but traditional banks can make this hard, especially for high-risk industries. In many cases, if you have an IT company and you go...

Lisbon, Portugal – PayDo, a leading payment ecosystem, is thrilled to announce its nomination for the prestigious “Payment Innovation of the Year” award at the SBC Awards 2024. The event...

There are three facts you need to know about PayDo: While those are all words, here are actual aspects making PayDo a standout EMI. What we want to do here...

A Merchant ID, or MID, is a unique identifier assigned to a business by its payment processor or acquiring bank when it starts accepting card payments. This ID is key...

All companies want to know the answer. They know buyers will pay for their goods, not just in cash. So, it is vital to set up credit card and mobile...

Small and Medium-Sized Enterprises (SMEs) are businesses with limited employees and revenue. They form the backbone of the global economy, driving growth, innovation, and employment. In Europe alone, SMEs account...

Phishing attacks are the most widespread forms of cybercrime. According to Cisco’s 2021 Cybersecurity Threat Trends Report, phishing attacks constitute over 90% of all data breaches. This number is much...

A payment gateway is critical in facilitating smooth and secure online transactions. They act as intermediaries between merchants and customers, ensuring that payment data is transferred securely and efficiently. As...

iGaming payment processing impacts the operator’s bottom line and the player’s experience. With a diverse global user base, iGaming platforms must support various payment methods and ensure fast, secure transactions...

Crafting a thriving business involves establishing a versatile payment infrastructure capable of receiving customer payments and facilitating sales regardless of time and location constraints. But what about scenarios where conventional...

In 2024, retail e-commerce sales exceeded $5.7 trillion globally. Any digital market out there can have a piece of that pie. This figure is expected to reach new heights in...

The increased use of phones and computers for transactions has led to new safety measures like 3D-Secure (3DS). A report by Grand View Research found that this market was worth...

Every day, Visa vs Mastercard process millions of payments. Naturally, when there are two main choices, people wonder: what is the difference between VISA and Mastercard debit card? Or, which...

In the previous article, we looked at ways to create a payment gateway for iGaming. In this piece, let’s take the next step – determine how to integrate such a...

Electronic Money Institutions (EMIs) and Money Services Businesses (MSBs) are becoming more and more popular. EMIs focus on digital transactions, providing electronic payment services and digital currency storage. According to...

Having a merchant account means small businesses can accept different types of payments online, like credit and debit cards, which most people use for online shopping. According to the Digital...

In days of electronic everything, you would think that most businesses wouldn’t longer use paper checks. Consumers have certainly ditched the paper check, with only 7% of their bills connected...

In the previous article, we took an in-depth look at the evolution of iGaming payments. In this piece, we take the next step. We plunge into the world of iGaming...

A Money Services Business (MSB) is a type of financial institution that offers various money-related services, such as money transfers, currency exchange, and check cashing. It is something similar to...

The International Bank Account Number (IBAN) was originally adopted by the European Committee for Banking Standards (ECBS) in 1997 as the international standard ISO 13616 under the International Organization for...

Electronic Money Institutions, or EMIs for short, are a simple way to send and receive money. These platforms are gaining popularity for opening a business account and setting up digital...

An Electronic Money Institution (EMI) is a financial institution that provides electronic payment services and digital currency storage. Unlike traditional banks, EMIs do not offer loans or other traditional banking...

Whether you’re running an online casino, sportsbook, or any other gaming platform, ensuring your players can deposit and withdraw funds seamlessly is crucial. A reliable payment gateway is the backbone...

By 2030, the global iGaming market is expected to reach $153 billion, driven by increasing digital infrastructure and the growing adoption of smartphones. This rapid growth underscores the critical role...

PayDo is an innovative Electronic Money Institution (EMI) that provides a wide range of financial solutions for both businesses and individuals. With its advanced platform, the platform offers a seamless...

Creating a PayDo business account is the first step. It lets you access a basic set of financial tools to streamline your business. To get all the features of your...

PayDo is a top-tier (I) Electronic Money Institution (EMI) and (II) Money Services Business (MSB) fully authorized by the (III) Financial Conduct Authority (FCA) in the United Kingdom and the...

According to Forbes, more than 53% of people in the US use digital wallets more than traditional payment methods. With the technology gaining popularity, new digital wallets emerge every week....

In 2022, there were around 3.4 billion digital wallet users around the world, 42% of humanity. By 2026, the number is expected to reach 5.2 billion or 60% of all...

Many people use digital wallets. The latest survey by Juniper Research predicts that digital wallets will be used to transact over $16 trillion in payments by 2028, compared to just...

Is PayDo safe? There is an important question to answer. We know the world of finance is a turbulent one. That’s why at PayDo, we’ve made safety and security our...

At PayDo, we’re not just about payments – we prioritize people above all else. That’s why we’re honored to announce our donation of €20,000 to two incredible charity organizations: Dream...

Experts regard the Danish market for its innovative payment processing schemes, which creates a unique opportunity for businesses to expand. Danes use Dankort all over the world. And mobile payment...

As per GlobeNewsWire, the market size for money transfer services is expected to exceed approximately US$ 110.8 billion by 2032. The growth is anticipated to follow a consistent Compound Annual...

Open Banking is breaking down traditional barriers between banks and financial institutions. Customers can now securely share a merchant’s banking information with trusted third parties. These include fintech service providers,...

When it comes to growing globally, businesses need to use localised checkout payment methods. This can help businesses build customer trust and position them for long-term success in the competitive...

World gambling statistics show that approximately 26% of the global population gambles. By 2025, the online gaming audience is expected to exceed 1.3 billion. The industry will continue booming in...

The online gambling industry is booming like never before. Research & Markets predicts that its global value will double from 2022 to 2028, hitting over $213 billion. No wonder everyone...

In 2022, the online gambling market was valued at $81.08 billion. It’s projected to increase to $88.65 billion by the end of 2023, with an annual growth rate of 9.3%. The...

Safeguarding international payments against payment fraud is paramount to the stability and efficiency of the global economy. Ensuring these transactions are secure and trustworthy allows businesses and individuals to operate...

Virtual terminals are web-based system that allows merchants to manually enter and process credit card transactions on a computer instead of using a physical point-of-sale (POS) system or terminal. Virtual...

Embedded finance refers to integrating financial services into non-financial platforms, applications, or processes. It represents a paradigm shift in how financial products are offered and consumed. Rather than the end-user...

IBAN account number discrimination is a financial practice where companies or organisations refuse to accept IBANs from other countries within the Single Euro Payments Area (SEPA). As more and more...

The International Bank Account Number (IBAN) has become a cornerstone for international transfers. According to Bankrate, digital banking is a growing trend. 76% of Americans using digital banking channels at...

The number of payment options as a part of checkout solutions is genuinely astonishing. Many choices exist, from standard credit cards to new open banking systems. Yet, not all of...

According to a report by MarketsandMarkets, the global digital payment market size will grow from $79.3 billion in 2020 to $154.1 billion by 2025. The increasing integration of advanced solutions...

With technology’s growth, businesses can operate globally without a physical base. Though they can serve customers everywhere, opening business accounts presents challenges. Traditional banks often demand a physical presence, complicating...

Many businesses want a basic account, but traditional banks can make this hard, especially for newer or unique sectors. This has made online payment platforms popular. They offer simple banking...

Can you guess how many freelancers are out there? Well, according to World Bank data, almost 47% of workers worldwide are freelancers. And if you are reading this article, chances...

Online gambling has already become not only fun, but also a global business, that encompasses all the world. For 2021, the global online gambling market is estimated at $ 72.02...

With the introduction of the global international bank account number (IBAN), which was implemented based on EC Regulation 2560/2001 and the European Committee on Banking Standards (ECBS), all banks and...

When sending or expecting money from abroad to a UK bank account, just giving the regular account number won’t do. You’ll usually need to provide more details, like an IBAN...

According to Forrester, by 2027, retail sales in the United States alone can reach a whopping $5.5 trillion. In addition, as per the Research and Markets report, global retail sales...