Crafting a thriving business involves establishing a versatile payment infrastructure capable of receiving customer payments and facilitating sales regardless of time and location constraints. But what about scenarios where conventional payment terminals are inaccessible? It is the moment when a virtual terminal comes into play.

The virtual payment terminals market is set to grow in the coming years. It is expected to reach a whopping $57.91 billion by 2028, with an impressive annual growth rate of 33.6%.

This growth is driven by several key factors. These are rapid technological advancements, a growing focus on environmental sustainability, the popularity of subscription-based services, increasing globalisation, and the need for enhanced security and compliance measures.

In this discussion, we look into the concept of virtual terminals, their functionality, the circumstances warranting their use, and the essential steps for setting one up, particularly for PayDo users.

What Is a Virtual Terminal?

The technology in question helps handle digital payments made over the phone, through mail, fax, email, or in person.

For example, in 2021, digital payments increased by 12%, according to McKinsey’s 2021 Digital Payments Consumer Survey. This growth in digital payments is expected to make virtual payment terminals more in demand.

Imagine a terminal as your digital cash register. It’s a tool that allows you to process customer payments without needing a physical card reader or terminal. Instead of swiping or inserting cards, you manually enter payment details like credit card numbers using your computer, tablet, or smartphone.

Here’s the thing: in the real world of business, there are times when you can’t rely on traditional payment methods. For instance, if you’re at a trade show, conducting business from your home office, or offering services on the go, you may not always have access to a regular point-of-sale system.

That’s where a digital terminal becomes your best friend. Picture this: a potential customer approaches you at a trade show and wants to buy your product or service immediately. With a virtual terminal, you can securely process their payment using your tablet or laptop without physical equipment.

Moreover, a virtual terminal lets you send invoices with payment links directly to your clients if your business provides services remotely, such as consulting or freelancing. They can conveniently pay online using their credit or debit cards, no matter where they are.

In essence, a virtual terminal acts as your portable payment hub. They provide the flexibility and convenience to accept payments anytime, anywhere. Especially in today’s dynamic business landscape.

Which Types of Businesses Use Virtual Terminal?

Virtual terminals are utilised by a variety of businesses across different industries. Here are some examples:

Service-based businesses

Freelancers, consultants, coaches, therapists, and professionals who offer services remotely or on the go often use virtual terminals to accept client payments.

E-commerce businesses

Online stores and businesses selling goods and products use virtual terminals to process payments for orders on their websites.

Mobile businesses

Global mobile payments are projected to experience a CAGR of 36.2% from 2023 to 2030. This indicates a substantial increase in the overall value of mobile transactions worldwide during this period.

Businesses that operate at events, trade shows, markets, or pop-up shops rely on virtual terminals to accept payments on the spot.

Telephone or mail-order businesses

Companies receiving orders over the phone or through mail order catalogs can use virtual terminals to enter payment details and process transactions manually.

Any business needing a flexible and convenient way to accept payments without relying solely on traditional point-of-sale systems or physical card readers can benefit from virtual terminals.

How Virtual Terminals Operate

Starting with a virtual terminal is straightforward. Depending on your merchant account provider, the process involves:

- Accessing an online dashboard or payment gateway to launch the virtual terminal.

- Choosing the payment method, whether credit/debit or eCheck/ACH.

- Entering the sales amount and any additional order notes.

- Manually input the card number or bank account details into the online form and any required billing information. Alternatively, if you have a USB card reader, you can swipe or insert the card at this stage.

- Clicking a button to initiate the transaction.

- Receiving confirmation of card approval or decline. In case of approval, most virtual terminals offer the option to email the client a copy of the receipt.

Besides processing payments, virtual terminals allow you to issue refunds and review your transaction history.

Benefits of Using Virtual Terminals

Here are some benefits for merchants when using virtual terminals:

- Virtual terminals allow merchants to process payments from anywhere with an internet connection. Whether in your office, at a trade show, or working remotely, you can accept payments seamlessly.

- Merchants can easily handle phone or email orders by manually entering payment details into the virtual terminal. This flexibility is especially useful for businesses that receive orders by phone or mail.

- With virtual terminals, merchants can cater to customers who prefer phone or email orders. This widens the customer base and increases sales opportunities.

- Virtual terminals streamline the payment process, allowing merchants to close sales swiftly. Customers appreciate the convenience of making payments without visiting a physical store.

- Merchants must adhere to Payment Card Industry Data Security Standard (PCI DSS) guidelines. Virtual terminals ensure the secure handling of sensitive customer data during transactions.

- Some virtual terminal providers use tokenisation, replacing card data with unique tokens. This adds an extra layer of security.

- Merchants can access detailed transaction records, including date, time, amount, and customer information. This helps with reconciliation and tracking.

- Virtual terminals provide analytics and reporting features, allowing merchants to analyse sales trends and make informed decisions.

Depending on the chosen payment gateway, merchants can offer customers more payment options, such as subscriptions or other forms of recurring payments, to capture their interest.

Offering protection for both buyers and sellers, as all customer credit card numbers undergo real-time verification. The payment gateway remains responsible for setting transaction security levels and reducing the burden on sellers. This is advantageous for small businesses and startups, as it allows for faster product launches without concerns about data security and payment processes.

Summing Up

The virtual terminal is a step towards the digital future that eliminates manual tasks and fully automates your business.

Looking ahead, we can expect to see partnerships and integrations becoming more common, subscription and service-based models gaining traction, cross-border payments becoming more seamless, ongoing technological advancements, and continuous innovation in product offerings.

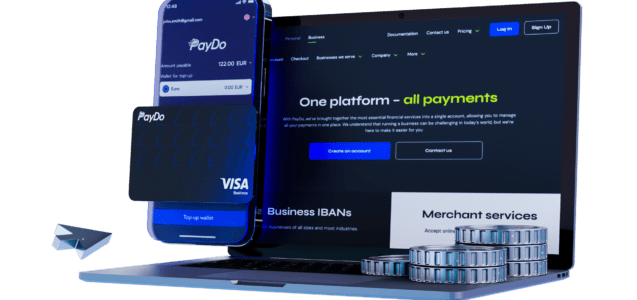

At PayDo, we’ve covered you with various features designed to meet your needs. With our platform, you can enjoy fully remote onboarding and multi-currency services supported by our live foreign exchange desk and activate your payment account in just minutes.

Our global network ensures real-time tracking of payments, and you can seamlessly pay and receive funds in foreign markets, just like local companies, making transfers both cost-effective and speedy.

Ready to step up? Then create your business account and enjoy the benefits of using PayDo for your business transactions.