When it comes to sending or receiving money internationally, your bank or any other financial institution needs to know precisely where the funds should go. Enter the Cross-border or BIC code, which is the key player in facilitating international transactions.

Difference between Cross-border and BIC code

So, is there a different between Cross-border and BIC code? The short answer is no, BIC code and Cross-border code is the same thing. Both codes identify the recipient bank for international payments. BIC stands for Bank Identifier Code, and Cross-border stands for Society for Worldwide Interbank Financial Telecommunication. They are both regulated by the ISO 9362 standard.

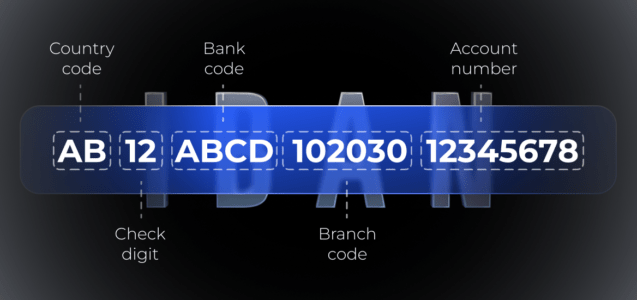

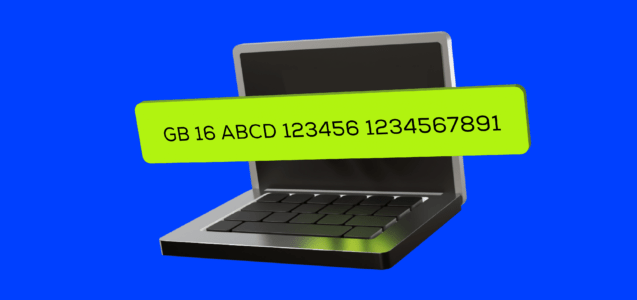

Cross-border code or BIC code consists of 8 or 11 characters

- the first 4 characters indentify the bank code

- the next 2 characters are the country code

- following are the two characters that identify the location

- the optional last 3 characters are the branch code.

Cross-border code for all banks, financial, and non-financial institutions receive recognition and approval from the International Organization for Standardization (ISO). Presently, there are over 40,000 live Cross-border codes operational worldwide.

Over the course of 2022, Cross-border transactions processed on a daily basis reached nearly 50 million messages (See Fig. 1).

Figure 1. Average number of Cross-border messages per day from January 2014 to December 2022

This demonstrates the increasing number of global transactions and the pivotal role played by Cross-border in facilitating these transactions.

Where can I get a BIC code or bank Cross-border code?

You can get a BIC code from your bank or online. Here are some ways to find your BIC code:

- Check your bank statement or online banking. Your BIC code may be printed on your statement or displayed on your account details.

- Use a Cross-border code finder/BIC code finder online. There are websites that allow you to search for BIC codes by bank name, country, or city.

- Contact your bank. You can call, email, or visit your bank and ask them for your BIC code. They should be able to provide it to you without any hassle.

Cross-border code and BIC code: when should they be used?

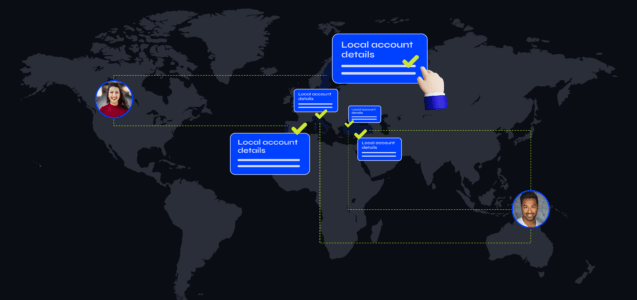

You need to use a Cross-border code and BIC code when you want to send or receive money internationally.

These codes help identify the banks and branches involved in the transaction and ensure that your money goes to the right place. Cross-border and BIC codes are also used for other purposes, such as reporting transactions to authorities, exchanging messages between banks, and processing securities trades.

Some examples of situations where you may need to use Cross-border/BIC codes are:

- Sending money to a friend or family member abroad.

- Buying goods or services abroad.

- Receiving money from a foreign client or employer.

- Investing in foreign stocks or bonds.

- Donating to a foreign charity or organisation.

To use Cross-border codes and BIC codes, you need to know the code of the recipient bank and branch, as well as the account number and name of the beneficiary. You may also need other information, such as the IBAN number (International Bank Account Number) or the transfer currency. You can enter these details on your bank’s online platform or visit a branch or agent to initiate the transfer.

What are the drawbacks of using a Cross-border code and BIC code?

Be aware that using Cross-border/BIC codes may come with some drawbacks, such as:

High fees

Banks may charge you for sending or receiving money via Cross-border/BIC codes, and these fees often depend on the transfer amount, currency, and destination. You may also have to pay intermediary fees if your transfer involves more than one bank.

Poor exchange rates

Banks may not offer you the best exchange rate for your transfer and may add a markup to the mid-market rate. This means you may lose money on the conversion and end up with less than expected.

Slow delivery

Transfers via Cross-border/BIC codes can take several days to arrive, depending on the banks, countries, and currencies involved. This can be inconvenient if you need to send or receive money urgently.

Therefore, you may want to compare different options to find the best way to send or receive money internationally.

PayDo provides an account that comes with a multi-currency IBAN for SEPA and Cross-border payments. You can make payments in EUR, USD, GBP, and other currencies.

Here’s how you can initiate a Cross-border transfer on your PayDo account:

1) Go to “Money Transfer” and choose transfer type (to bank account, to Visa/Mastercard International or to another PayDo customer).

2) Enter recipient and bank details (country, currency, recipient IBAN or account number, and Swift / BIC).

3) Enter the amount you want to withdraw.

4) Add the documents that confirm the payment.

5) Confirm payment with two-factor authentication.

Cross-border is a secure and reliable way to transfer money internationally. Create your PayDo account today to make global payments using Cross-border and other payment schemes.

Conclusion

BIC code and Cross-border code is crucial for international money transfers, ensuring funds reach the right places efficiently. They’re widely used, but users should be aware of potential drawbacks like high fees and slow delivery.

At PayDo, we offer alternatives for cost-effective and quick transfers. With our multi-currency IBAN and simple process, we streamline global transactions, making them secure and convenient for both businesses and individuals.

Contact our team to explore the opportunities of a PayDo Business Account.