Electronic Money Institutions (EMIs) and Money Services Businesses (MSBs) are becoming more and more popular. EMIs focus on digital transactions, providing electronic payment services and digital currency storage. According to the European Central Bank, electronic money transactions in the euro area totaled €111 billion in 2024, reflecting the growing adoption of EMIs.

On the other hand, MSBs offer essential financial services such as money transfers and currency exchanges. With over 30,000 registered MSBs in the United States alone, as reported by FinCEN, their role in promoting financial inclusion cannot be overstated.

EMIs and MSBs are transforming how individuals and businesses handle money, offering more accessible and efficient alternatives to traditional banking. This transformation is about meeting the evolving needs of a globalized economy and enhancing financial inclusion for all.

So, it is time to take a closer look on both EMIs and MSBs.

What is an EMI?

An Electronic Money Institution (EMI) is a financial entity that provides electronic payment services and digital currency storage. Unlike traditional banks, EMIs do not offer loans or conventional banking services but focus on facilitating electronic transactions. They enable users to make online payments and transfers and store digital money securely.

The core functions of EMIs include issuing electronic money, managing digital wallets, and processing online payments efficiently. EMIs are regulated entities, ensuring they comply with stringent financial regulations to protect consumers and maintain the integrity of digital transactions. For example, in the UK, EMIs are regulated by the Financial Conduct Authority (FCA), which oversees their operations to ensure they adhere to industry standards and safeguard user funds.

Use Cases

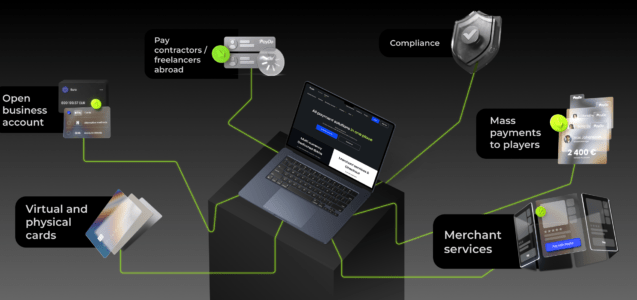

Popular EMIs include companies like PayDo, which offer various digital financial services. Use cases for EMIs are extensive and varied. For instance, consumers can use EMI services to make instant payments directly from their digital wallets during online shopping.

Businesses leverage EMIs for international money transfers, enabling them to send and receive payments quickly and efficiently across borders. Additionally, EMIs facilitate business transactions by providing multicurrency accounts and comprehensive payment solutions, streamlining operations for companies engaging in global commerce.

For more details, you can refer to this piece.

What is an MSB?

A Money Services Business (MSB) is a financial entity that provides various money-related services to the public. Unlike traditional banks, MSBs focus on accessible financial services such as money transfers, currency exchange, and check cashing. These businesses are crucial in offering financial services to individuals needing access to conventional banking.

The primary services offered by MSBs include:

- Money Transfers. Enabling individuals to send money domestically and internationally.

- Currency Exchange. Allowing people to convert one currency into another is especially useful for travelers.

- Check Cashing. Allowing individuals to cash checks without needing a bank account.

MSBs are subject to stringent regulatory requirements, including Anti-Money Laundering (AML) and Know Your Customer (KYC) compliance. These regulations ensure that MSBs operate transparently, prevent financial crimes, and protect consumers. MSBs must verify the identity of their customers, monitor transactions for suspicious activity, and maintain detailed records to comply with these regulations.

Use Cases

Well-known examples of MSBs include Western Union and MoneyGram, widely recognized for their money transfer services. Everyday use cases for MSBs include:

- Remittance Services. Migrant workers use MSBs to send money back home to support their families.

- Currency Exchanges for Travelers. Travelers use MSBs to exchange currency when visiting foreign countries.

- Check Cashing. Individuals without bank accounts rely on MSBs to quickly cash payroll or government-issued checks.

For more details, you can refer to this article.

Seven Key Differences

Understanding the distinctions between electronic money institutions (EMIs) and money services businesses (MSBs) is crucial for companies and individuals who want to choose the right financial services. Here are seven key differences to consider:

1. Regulatory Framework

EMIs are regulated by U.K. entities like the Financial Conduct Authority (FCA), focusing on digital money issuance and electronic transactions. MSBs must comply with broader financial regulations, including AML and KYC requirements imposed by bodies like FinCEN in the U.S.

2. Services Offered

EMIs provide services such as digital wallets, online payments, multicurrency accounts, and international transfers. MSBs offer money transfers, currency exchange, check cashing, and the issuance of traveler’s checks and money orders.

3. Target Audience

EMIs primarily serve digitally savvy consumers, e-commerce businesses, and tech startups. In contrast, MSBs cater to the general public, including unbanked and underbanked individuals, as well as businesses requiring physical money services.

4. Technological Integration

EMIs often provide APIs for seamless integration with e-commerce platforms, ensuring smooth digital transactions. MSBs might use more traditional methods, though many are adopting digital solutions to enhance service delivery.

5. Security and Compliance

EMIs must comply with PCI DSS for secure card transactions, employing encryption and multifactor authentication. MSBs focus on AML and KYC compliance to prevent financial crimes, requiring customer verification and transaction monitoring.

6. Cost and Fees

EMIs typically offer competitive rates for international transactions, leveraging digital platforms to reduce costs. MSBs might have higher fees due to the operational costs of physical locations and services.

7. Speed of Transactions

EMIs provide instant or near-instant digital transactions, enhancing business efficiency. MSBs may have longer processing times, especially for international transfers and currency exchanges.

By understanding these differences, businesses and individuals can make more informed decisions about which type of financial service best suits their needs.

Conclusion

Understanding the differences between EMIs and MSBs is essential for selecting the right financial services. EMIs focus on digital transactions, offering services like digital wallets, online payments, and international transfers, while MSBs provide money transfers, currency exchange, and check cashing. The regulatory frameworks, target audiences, technological integration, security measures, cost structures, and transaction speeds vary significantly between the two.

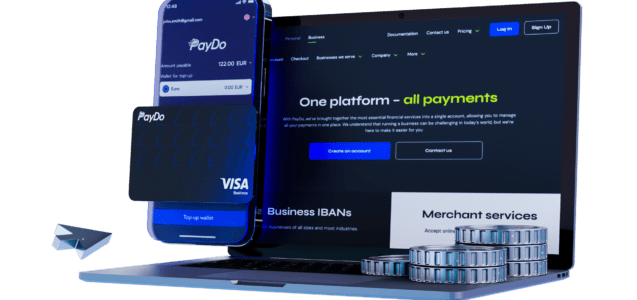

Choosing the right type of service depends on your specific business or personal needs. For companies looking to streamline digital payments and manage international transactions efficiently, an EMI like PayDo is an ideal choice. For individuals and businesses needing accessible financial services like currency exchange or remittance, MSBs provide valuable solutions.

At PayDo, we offer a comprehensive suite of EMI services designed to meet modern financial needs with security and efficiency. Explore our services to find the perfect solution for your payment requirements.

Create your PayDo Business or PayDo Personal account today to experience seamless financial transactions and enhance your financial operations.