The increased use of phones and computers for transactions has led to new safety measures like 3D-Secure (3DS). A report by Grand View Research found that this market was worth $1.1 billion in 2022. And it is expected to grow at 12.7% CAGR from 2023 to 2030.

Businesses need a system that works well with what they already use, keeps payments safe, and makes paying easier. Let’s talk about 3D-Secure. We will explore how it works and how businesses can use it to improve their customer payment systems.

The Definition of 3D-Secure

A 3D-Secure protocol adds an additional layer of security to online transactions involving credit and debit cards.

Before completing the payment, it verifies the cardholder’s identity via a password, a PIN, or a biometric factor. The term 3DS comes from the three parties involved: the cardholder, the issuing bank, and the merchant.

3DS version 1.0 was initially introduced in the early 2000s. Later, version 2.0 came to life. It includes enhancements like support for mobile payments and biometric authentication. All to improve the user experience. And reduce the number of transaction abandonments due to verification complexity.

Is it mandatory to use 3D-Secure for online transactions?

3D-Secure is not mandatory for all online transactions. But it may be a requirement or recommendation in some cases. For example:

- In the European Union, the Payment Services Directive 2 (PSD2) requires strong customer authentication (SCA).

- Some card issuers may enforce 3D Secure for certain transactions. All based on their risk assessment or offer incentives for cardholders to use it.

- Some merchants may choose to implement 3D Secure on their checkout pages to reduce fraud and chargebacks or comply with card network security standards, such as Visa and Mastercard.

According to Visa, the improved 3DS protocol (3D Secure 2) is going to cut down the cart abandonment rate by 70% and make checkout faster by 85%. Now, let’s explore how 3DS works.

How Does 3DS Work?

The 3D Secure process is a series of steps involving different parties to make online transactions safer. Each step plays a part in making sure the authentication system works well.

This protocol relies on three main parts: the card issuer, the acquirer, and the interoperability domain. Let’s look at each step in detail.

- The customer enters their card details on the merchant’s website and clicks “Pay”.

- The merchant’s server sends a request to the acquirer, the bank that processes the merchant’s card transactions.

- The acquirer forwards the request to the card scheme, which is the network that connects card issuers and acquirers, such as Visa or Mastercard.

- The card scheme checks if the card is enrolled in 3D Secure and sends a response to the acquirer.

- The acquirer sends the response to the merchant’s server, determining whether 3D Secure authentication is required.

- If 3D Secure authentication is required, the merchant’s server redirects the customer to the issuer’s 3D Secure web page or app, where they have to provide additional verification, such as a password, a PIN, or a biometric factor.

- The issuer verifies the customer’s identity and responds to the card scheme, indicating whether or not the authentication was successful.

- The card scheme sends the response to the acquirer, which forwards it to the merchant’s server.

- The merchant’s server completes the payment process if the authentication is successful or displays an error message if it is not.

Even though it seems like a lot is going on, the 3D Secure authentication process usually takes a few seconds to complete. The speed may be slower, depending on the internet connection speed and the verification method.

Factors causing delays and errors

However, some factors may cause delays or errors, such as:

- The cardholder does not have 3D Secure enabled on their card or has not registered for it.

- The cardholder enters the wrong password, PIN, or biometric factor or does not respond to the verification prompt in time.

- The card issuer’s 3D Secure web page or app is not working properly or is incompatible with the customer’s device or browser.

- The card scheme, the acquirer, or the merchant’s server experiences technical issues or network failures.

To avoid these issues, cardholders check with their card issuers if they have 3D Secure enabled and how to register for it. They should also use a reliable internet connection and a compatible device and browser when making online payments.

Additionally, they should follow the instructions on the 3D Secure web page or app carefully

and enter the verification information correctly and promptly.

3DS helps to reduce the likelihood of fraud with stolen card details, as a fraudster would need to pass through additional layers of verification to make a purchase.

Benefits of 3DS

Overall, 3DS helps to reduce the likelihood of fraud with stolen card details, as a fraudster would need to pass through additional layers of verification to make a purchase. However, it can provide several benefits for both merchants and customers, such as:

Lower risk of fraud and chargebacks

3D Secure can help to verify the identity of the cardholder and prevent unauthorised transactions. This can reduce the costs and losses associated with fraud and chargebacks.

Increased customer confidence and loyalty

3D Secure can enhance the trust and satisfaction of customers who shop online, as they can feel more secure and protected. This can encourage them to make more purchases and become loyal customers.

Compliance with regulations and standards

3D Secure can help merchants and issuers comply with the Payment Services Directive 2 (PSD2) in Europe, which requires strong customer authentication for online card transactions. It can also help them meet the security standards of card networks, such as Visa and Mastercard.

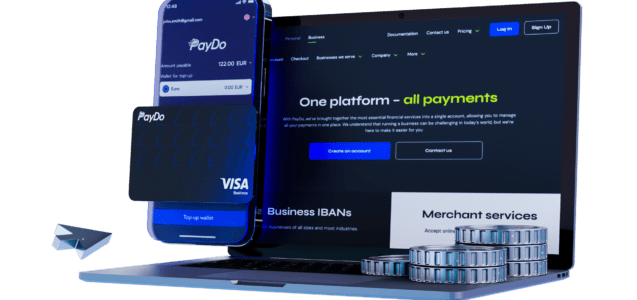

If you are a merchant and looking for a reliable EMI that is 3DS compliant, PayDo is the way to go. All card payments within the system are protected by 3D Secure, adding an extra layer of security.

With a PayDo Merchant Account, you can enter new markets and process payments with major and local payment methods across the globe.

Our checkout ensures smooth online purchases as well as a secure and efficient payment infrastructure.

Summing Up

3D Secure makes online payments safer by adding an extra check. Normally, when you buy something online, you just enter your card details and security code. But with 3D Secure, you might also need to enter a password or get a special code sent to your phone. This extra step happens in a pop-up window or within an app.

For merchants seeking a reliable Electronic Money Institution (EMI) compliant with 3D Secure, PayDo offers a solution ensuring secure transactions and facilitating global payment processing across major and local payment methods.

With a PayDo Merchant Account, businesses can expand into new markets while ensuring smooth and secure online purchases backed by an efficient payment infrastructure.

Contact us to learn more about what we offer for e-commerce solutions and other businesses.