An Electronic Money Institution (EMI) is a financial institution that provides electronic payment services and digital currency storage. Unlike traditional banks, EMIs do not offer loans or other traditional banking services but instead focus on facilitating electronic transactions and providing digital wallets. EMIs must have authorisation to issue electronic money and manage digital transactions.

According to a European Central Bank report, electronic money transactions in the euro area total €111 billion in 2024, demonstrating a significant increase from previous years. This growth highlights the expanding influence and adoption of EMIs in the financial sector.

“EMIs are transforming the landscape of financial transactions by offering unparalleled convenience and security. They meet the evolving needs of businesses and consumers alike,” says Alexander Persidsky, Head of Operations at PayDo.

In this article, let’s learn more about what EMI means and what it is like.

Understanding Electronic Money Institution (EMI)

EMIs issue electronic money and facilitate digital transactions, enabling users to perform online payments, transfers, and other financial activities without needing physical cash or traditional banking services.

EMIs differ from traditional banks in several key ways:

- Digital-First. Unlike banks, which offer various financial services, including loans, mortgages, and savings accounts, EMIs concentrate on digital payment solutions. They provide platforms for storing and transferring electronic money, making them ideal for online transactions.

- No Lending Services. EMIs do not offer loans or credit services. Their primary function is to manage electronic payments and digital wallets.

- Regulatory Framework. While both EMIs and banks are regulated, EMIs are often subject to specific regulations tailored to electronic money and digital transactions.

Key Characteristics of an Electronic Money Institution (EMI)

- Focus on Digital Transactions. EMIs handle online and digital payments efficiently. For instance, when you use PayDo to pay for an online purchase, the system instantly processes a transaction through its digital platform, ensuring a seamless payment experience.

- Provision of Electronic Money Instead of Traditional Banking Services. EMIs issue electronic money that can be used for various transactions. Unlike physical cash or checks, electronic money is stored digitally and can be transferred instantly. For example, PayDo allows businesses to receive payments from international clients without the delays associated with traditional bank transfers.

Examples to Understand Electronic Money Institutions (EMIs) Better

- Online Shopping. The payment is processed through your digital wallet when you buy something online using EMIs like PayDo. This is quicker and more efficient than a traditional bank transfer, which may take several days to clear.

- International Transfers. Suppose you need to send money to a friend abroad. Using an EMI like PayDo, you can transfer funds instantly, avoiding the high fees and lengthy processing times typically associated with bank wire transfers.

Advantages of Using an EMI

- Real-Time Processing and Access to Multiple Currencies. One of the main advantages of using an EMI is the ability to process transactions in real time. Users can send and receive money instantly, avoiding the delays commonly associated with traditional banking.

- Reduced Fees for International Transactions Compared to Traditional Banks. EMIs typically offer lower transaction fees compared to traditional banks, especially for international payments. This cost efficiency makes EMIs an attractive option for individuals and businesses looking to minimize their financial expenses while maximizing their transaction capabilities.

- Compliance with PCI DSS and Other Security Standards. EMIs comply with PCI DSS Level 1 standards, ensuring that all card transactions are secure and protected against fraud. Additionally, EMIs can employ advanced encryption technologies and multi-factor authentication to safeguard user data. For instance, when a user tops up their PayDo account, 3D-Secure (3DS) authentication adds an extra layer of security, verifying the transaction and preventing unauthorized access.

By offering these core functions and advantages, EMIs change the financial landscape for the better. They provide users with efficient, secure, cost-effective solutions for managing digital transactions.

Conclusion

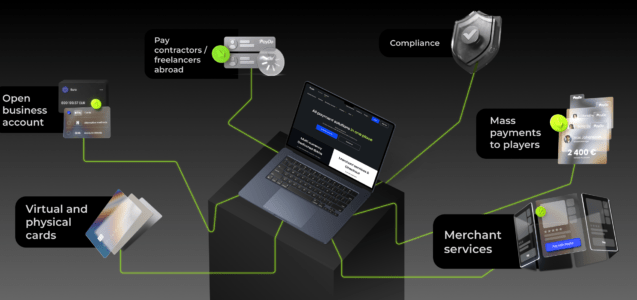

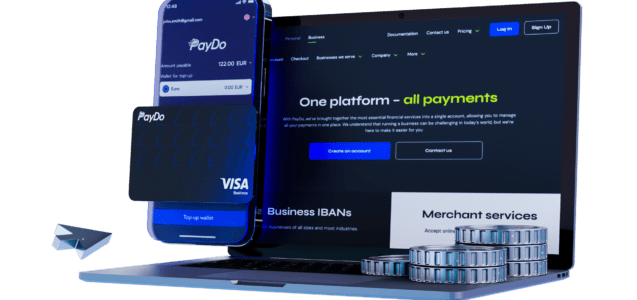

EMIs are reshaping the financial landscape by offering innovative digital payment solutions that are secure, efficient, and cost-effective. They provide personal and business accounts, merchant services, mass payments, and virtual and physical cards.

EMIs operate under strict regulatory frameworks, ensuring compliance with standards like PCI DSS and robust security measures such as 3D-Secure (3DS) and chargeback protection. They bridge the gap between traditional banking and modern digital finance.

Ready to start with one of the top-tier EMIs out there? Create PayDo Personal or PayDo Business Account for individual or corporate purposes. Tap into the convenience of financial transactions right away.